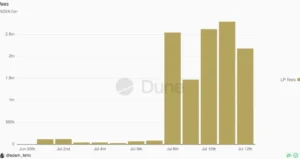

The nascent Robinhood Chain, which launched with significant fanfare earlier this month, has encountered its first major crisis following the abrupt cessation of operations by Noxa, its primary memecoin launchpad. On July 11, 2026, Noxa officials announced they would halt new token deployments, effectively ending a two-week period of unprecedented growth that saw the platform generate over $12 million in protocol fees. The departure of the ecosystem’s dominant infrastructure provider has sent shockwaves through the market, resulting in a sharp contraction of liquidity and a double-digit decline in the valuation of flagship assets.

Noxa’s influence on the Robinhood Chain cannot be overstated. Since the chain’s inception on July 1, 2026, the launchpad served as the primary gateway for retail speculation, facilitating the creation of over 60,000 unique tokens. At its peak, Noxa accounted for approximately 75% of all token deployments on the network, a level of concentration that left the ecosystem’s health heavily dependent on a single private entity. For five consecutive days leading up to its closure, Noxa’s daily protocol fees surpassed those of Pump.fun, the long-standing incumbent in the memecoin launchpad sector, marking a historic shift in decentralized finance (DeFi) activity.

The Rapid Ascent and Sudden Descent of Noxa

The rise of Noxa was inextricably linked to the broader "Robinhood Summer" narrative promoted by Robinhood CEO Vlad Tenev, who declared the season’s arrival on July 8. The chain was designed to bring the ease of use associated with the Robinhood brokerage app to the world of on-chain trading. Noxa capitalized on this by offering a streamlined, "one-click" launch mechanism that appealed to both sophisticated developers and retail novices.

This accessibility fueled a speculative frenzy that propelled the Robinhood Chain to a $4 billion cumulative decentralized exchange (DEX) volume milestone in less than 14 days. On July 12, just one day after Noxa announced its suspension of new launches, the chain’s daily DEX volume reached a record high of $878 million. However, the momentum proved unsustainable.

The first signs of trouble appeared on July 11, when Noxa’s leadership cited an "overwhelming flood of bot spam and low-quality token deployments" as the rationale for halting new activity. While the team initially framed the move as a temporary measure to protect the integrity of the ecosystem, the situation escalated on July 13 when the Noxa website went entirely dark. The team attributed the outage to a technical failure involving Cloudflare, but the lack of a clear recovery timeline triggered a wave of panic selling across the network.

Market Impact: The Fall of CASHCAT and Ecosystem Tokens

The immediate casualty of Noxa’s disappearance was CASHCAT, the Robinhood Chain’s flagship memecoin. CASHCAT had previously reached a peak market capitalization of $226 million, supported by a massive user base of 267,642 unique wallets. Following the news of Noxa’s shutdown, the token plummeted by more than 33% within a 24-hour window.

The contagion quickly spread to other prominent assets within the ecosystem. Tokens such as FOX and HOODIE, which had benefited from the massive influx of liquidity and visibility provided by Noxa’s interface, saw their valuations erode as investors scrambled to exit positions. This volatility underscored a critical vulnerability in the Robinhood Chain: the extreme concentration of volume and liquidity within a handful of memecoins launched via a single platform.

The instability was further exacerbated when a rival launchpad, Vlad.fun, also ceased operations just days later. The Vlad.fun team cited "internal integrity issues," a vague explanation that did little to soothe the nerves of a community already reeling from Noxa’s exit. The dual collapse of the chain’s two most popular launchpads created a vacuum that remaining competitors have struggled to fill.

A Chronology of the Robinhood Chain Crisis

To understand the scale of the current market disruption, it is necessary to examine the compressed timeline of events that led to the present state of the Robinhood Chain:

- July 1, 2026: Robinhood Chain officially goes live, targeting the intersection of retail finance and decentralized protocols.

- July 5, 2026: Noxa emerges as the dominant launchpad, capturing the majority of new token deployments and attracting tens of thousands of users.

- July 8, 2026: Robinhood CEO Vlad Tenev tweets "Robinhood Summer is here," driving a surge in social media engagement and capital inflows.

- July 10, 2026: Noxa records its fifth consecutive day of out-earning Pump.fun in protocol fees, with cumulative revenue exceeding $12 million.

- July 11, 2026: Noxa halts new token launches, citing the need to combat botting and low-quality "rug pull" projects.

- July 12, 2026: Robinhood Chain hits a peak daily DEX volume of $878 million; CASHCAT reaches its all-time high market cap.

- July 13, 2026: The Noxa website goes offline. The team blames Cloudflare issues, but community skepticism begins to mount.

- July 15, 2026: Noxa announces a pivot, stating it will redirect 100% of ongoing trading fees to token creators rather than retaining them as profit.

- July 17, 2026: Rival platform Vlad.fun shuts down, citing integrity concerns. Ecosystem-wide sell-offs intensify.

- July 18, 2026: Major crypto media outlets and analysts, including Coin Bureau, report on the $12 million fee collection and the subsequent disappearance of the platform.

Analysis of Noxa’s "Exit Strategy"

The decision by the Noxa team to redirect 100% of trading fees to token creators is perhaps the most unusual aspect of this episode. In traditional "rug pull" scenarios, developers typically vanish with all accumulated funds and protocol revenue. By walking away from a lucrative revenue stream while the chain was still seeing hundreds of millions in volume, the Noxa team has sparked a debate within the crypto community regarding their true motives.

Some observers, including prominent trader 0xAvast—who reportedly turned a $10,000 investment in CASHCAT into a multimillion-dollar position—have dismissed the concerns as "irrelevant FUD" (Fear, Uncertainty, and Doubt). These supporters argue that Noxa’s exit was an ethical, albeit clumsy, attempt to decentralize the ecosystem and prevent a total collapse driven by regulatory scrutiny or technical debt.

Conversely, a significant portion of the community views the move as a "soft rug." By collecting $12 million in fees and then disabling the primary engine of growth, the developers effectively capped the upside for retail investors while securing their own windfall. Critics argue that the redirecting of fees was a strategic move to mitigate legal liability rather than a benevolent gesture toward the community.

Broader Implications for the Robinhood Chain

The Noxa crisis has highlighted a stark disparity between Robinhood’s stated goals for its blockchain and the reality of its early adoption. The chain was built with the primary intention of hosting tokenized real-world assets (RWAs), such as stocks, bonds, and commodities. However, as of mid-July 2026, the total market capitalization of RWAs on the network stands at a mere $12.66 million.

In contrast, at its peak, the CASHCAT memecoin alone was valued at more than twelve times the entire RWA sector on the chain. This imbalance suggests that the "Robinhood Summer" was driven almost entirely by speculative mania rather than the institutional adoption of blockchain-based securities. The loss of Noxa, which provided the infrastructure for this speculation, now threatens the chain’s overall TVL (Total Value Locked), which has managed to hold steady near $200 million but remains at risk if a secondary migration occurs.

Efforts are underway by other platforms to capture the displaced volume. Launchpads such as flap.sh, trensh.today, bankr, and the newly launched Pons have seen a slight uptick in activity. However, none of these platforms currently possess the brand recognition or the "hit-making" track record of Noxa. Furthermore, the loss of investor confidence in the launchpad model on the Robinhood Chain may prove difficult to restore.

Conclusion and Market Outlook

The episode serves as a cautionary tale for the decentralized finance sector, particularly regarding the risks of infrastructure centralisation. When an entire ecosystem’s growth is funnelled through a single proprietary launchpad, the platform itself becomes a single point of failure. When that platform disappears—whether due to technical issues, regulatory pressure, or a strategic exit—it takes the market’s momentum with it.

For investors, the focus has shifted from finding the "next CASHCAT" to evaluating the long-term viability of the Robinhood Chain itself. If the network can successfully transition from memecoin speculation to its intended purpose of RWA tokenization, it may yet recover. However, in the short term, the shadow of Noxa’s $12 million exit looms large, reminding participants that in the world of high-speed crypto launches, the house almost always wins before the lights go out.

As the community monitors the 200 million dollars in TVL for signs of further flight, the primary question remains whether the Robinhood Chain can foster a more diversified and resilient infrastructure that does not rely on the whims of a single dominant player. For now, the "Robinhood Summer" has met a chilling autumn of uncertainty.

{kind=link}