Tradable, a prominent marketplace for private assets and a leading tokenization infrastructure provider, has officially announced a strategic partnership with the Stellar Development Foundation to migrate and issue up to $1 billion in tokenized private credit assets on the Stellar network. The announcement, made on July 15, marks a significant milestone in the ongoing evolution of Real World Assets (RWAs) within the blockchain ecosystem, signaling a deepened commitment from institutional players to utilize distributed ledger technology for traditional financial instruments. This collaboration aims to enhance the accessibility, liquidity, and transparency of private credit, a sector of the financial market that has historically been characterized by high barriers to entry and opaque settlement processes.

The decision by Tradable to utilize the Stellar blockchain is rooted in the network’s specific architecture, which was designed from its inception to facilitate the issuance and exchange of digital representations of value. By moving up to $1 billion in private credit assets onto the chain, Tradable is positioning itself at the forefront of the institutional RWA movement. This move follows a period of robust growth for Tradable, which has already successfully tokenized approximately $1.7 billion in assets across 30 distinct institutional-grade deals. The transition to Stellar represents an expansion of this existing portfolio, leveraging Stellar’s low-cost environment and specialized compliance tools to serve a global base of institutional investors.

The Strategic Shift Toward Tokenized Private Credit

Private credit involves non-bank lending where debt is not issued or traded on public markets. In the traditional financial landscape, this asset class is often lucrative but suffers from fragmentation and a lack of secondary market liquidity. Tokenization—the process of creating a digital twin of these credit assets on a blockchain—allows for fractional ownership, automated compliance through smart contracts, and near-instantaneous settlement. For institutional investors, these features reduce the administrative overhead associated with managing complex debt portfolios and provide a clearer audit trail of asset performance.

Tradable’s platform acts as the bridge between these traditional debt instruments and the blockchain. By selecting Stellar, Tradable is tapping into a network that has become a preferred destination for regulated financial institutions. Unlike general-purpose blockchains that may prioritize decentralized applications or gaming, Stellar’s development has remained focused on the movement of money and the tokenization of assets. This focus has resulted in a suite of built-in features, such as the Stellar Asset Contract and integrated compliance protocols (including KYC/AML hooks), which allow issuers to maintain strict regulatory oversight over their tokenized offerings.

A Chronology of Institutional Adoption and Growth

The partnership between Tradable and Stellar is the culmination of several years of development in the RWA sector. To understand the significance of this $1 billion commitment, it is necessary to examine the timeline of Tradable’s growth and Stellar’s ascent in the RWA rankings.

In 2025, Tradable reported a record year, reaching $1.7 billion in total tokenized value. This volume was driven by 30 major deals involving institutional investors who sought exposure to alternative assets through a digital-first lens. These early successes demonstrated that there was significant demand for on-chain credit, provided the underlying infrastructure could meet the rigorous standards of traditional finance.

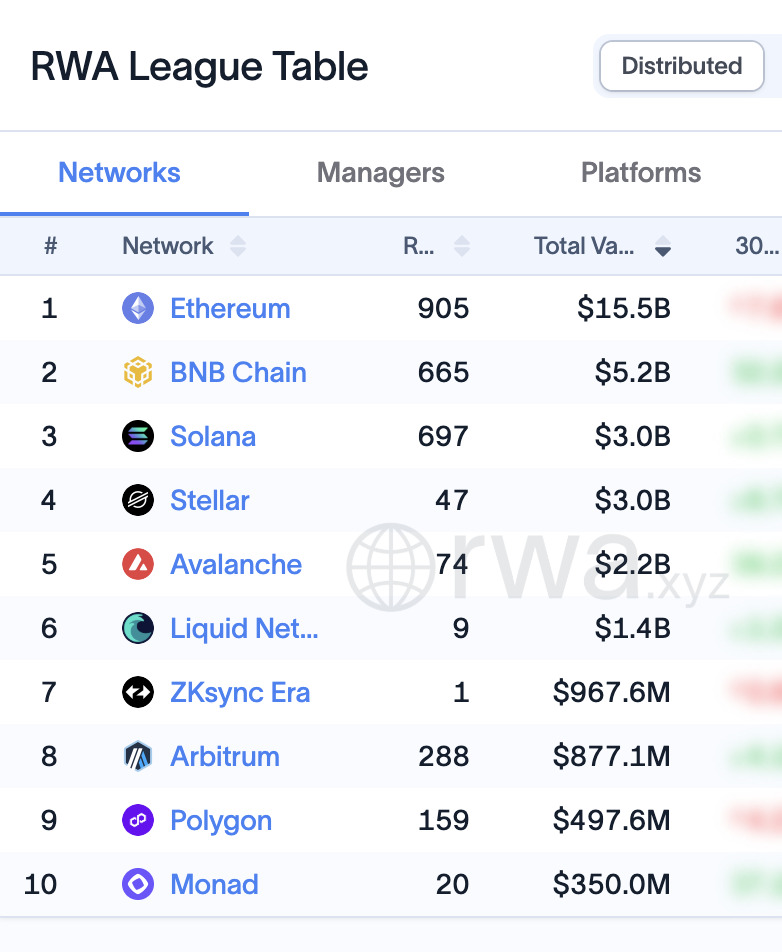

By mid-2026, the competitive landscape for RWA blockchains had solidified. According to data from RWA.xyz, an industry-leading analytics platform, the total value of RWAs across all major blockchains reached new heights, with Ethereum maintaining its lead and BNB Chain holding the second position. However, Stellar began to separate itself from the pack of "Ethereum killers" by focusing specifically on institutional debt and treasuries.

As of July 16, 2026, Stellar’s RWA ecosystem reached approximately $3 billion in total value, placing it 4th globally among all blockchains. The network’s growth has been accelerating; in the 30 days leading up to the Tradable announcement, Stellar saw a 6.8% increase in total RWA value and a staggering 29% increase in asset transfer volume, totaling $8.6 billion. This momentum provided the necessary proof of concept for Tradable to commit its next $1 billion in assets to the network.

Supporting Data: The Stellar RWA Ecosystem

The composition of assets currently on the Stellar network highlights why it is an attractive home for Tradable’s private credit portfolio. The network’s RWA value is diversified across several key financial categories:

- U.S. Treasury Debt: This remains the largest segment on Stellar, with over $1.2 billion in tokenized treasuries. These products offer investors a "risk-free" yield in a digital format, often used as collateral within the broader on-chain ecosystem.

- Active Management Strategies: Approximately $714 million is currently deployed in actively managed on-chain funds, where managers use blockchain transparency to report real-time performance to investors.

- Corporate Credit: This category, which directly aligns with Tradable’s core business, currently sits at $513 million. The influx of Tradable’s $1 billion will nearly triple the size of this segment, making Stellar a dominant force in the on-chain corporate debt market.

- International Government Debt: Stellar also hosts roughly $506 million in non-U.S. government debt, showcasing the network’s global reach.

The network’s success is also reflected in its list of major issuers. Spiko currently leads the network with $1.3 billion in tokenized assets, followed by Franklin Templeton’s Benji Investments at $583 million. Other major players include Ondo Finance, with $533 million, and Realiz, which manages $500 million. Tradable’s entry into this ecosystem with a $1 billion target places it among the top three largest issuers on the network, significantly altering the balance of power in the RWA landscape.

Furthermore, the "retail-institutional" bridge on Stellar is supported by a growing holder base. Currently, more than 18,000 unique addresses hold RWA tokens on Stellar, and the market capitalization of native stablecoins—which provide the necessary liquidity for these trades—is approaching $350 million.

Official Responses and Executive Perspectives

Leaders from both organizations have emphasized that this partnership is about more than just a large number; it is about the long-term infrastructure of global finance.

Alex Goldwater, CEO of Tradable, expressed confidence in the move, stating that the partnership allows the company to build the "next generation of alternative asset infrastructure." He noted that by deploying assets on Stellar, Tradable can ensure that its institutional clients benefit from the efficiency of blockchain while remaining within the bounds of traditional regulatory frameworks. Goldwater highlighted that the ability to offer secondary market liquidity for private credit is a "game-changer" for the industry.

Denelle Dixon, CEO of the Stellar Development Foundation, echoed these sentiments, framing the Tradable deal as a validation of Stellar’s long-term strategy. Dixon remarked that the decision by a firm like Tradable to bring $1 billion in assets to the network serves as a clear signal that enterprises are choosing Stellar as the foundation for large-scale, on-chain financial assets. She emphasized that Stellar’s design—optimizing for low fees and high throughput without sacrificing security—is exactly what institutional investors require to move away from legacy systems.

Broader Impact and Market Implications

The implications of Tradable’s $1 billion commitment extend far beyond the two companies involved. This move is indicative of a broader trend where the "tokenization of everything" is moving from a theoretical concept to a multi-billion dollar reality.

First, the deal intensifies the competition between blockchains for RWA dominance. While Ethereum currently holds the largest share of RWA value at $15.5 billion, its high transaction fees and network congestion often make it less ideal for high-volume, small-ticket credit transactions. Stellar, by positioning itself as a low-cost, compliance-heavy alternative, is successfully poaching institutional volume that might otherwise have gone to Layer 2 solutions or competing chains like Solana (which currently trails Stellar in certain corporate credit metrics).

Second, the move signals a maturation of the private credit market itself. As interest rates remain a focal point of global macroeconomics, investors are seeking higher-yielding alternatives to public equities and bonds. Private credit offers these yields, and tokenization removes the "liquidity discount" typically associated with these assets. If Tradable successfully tokenizes $1 billion on Stellar, it will likely prompt other private equity and credit firms to explore similar on-chain strategies.

Third, the regulatory clarity provided by the Stellar network’s built-in features is likely to attract more conservative institutional capital. The ability to program "clawback" features (the ability to recover tokens in the event of a lost key or legal dispute) and "freeze" functions (to prevent unauthorized transfers) addresses the primary security concerns of traditional fiduciaries.

In conclusion, the partnership between Tradable and Stellar represents a pivotal moment for the integration of blockchain technology into the $1.6 trillion global private credit market. By combining Tradable’s expertise in asset sourcing and institutional relations with Stellar’s purpose-built financial infrastructure, the two entities are setting a new benchmark for the scale and sophistication of Real World Assets on the blockchain. As the first tranches of this $1 billion commitment begin to go live, the financial industry will be watching closely to see if this model becomes the new standard for institutional debt issuance.

{kind=link}