The global financial landscape is currently undergoing a fundamental transformation driven by the emergence of Web3 and the integration of decentralized technologies. At the heart of this shift lies the concept of crypto assets—digital representations of value that operate independently of traditional banking systems and government oversight. Formerly referred to predominantly as "virtual currencies," these assets have evolved from niche experimental protocols into a multi-trillion-dollar asset class that defines the modern digital economy. However, as adoption increases, so does the necessity for a comprehensive understanding of the underlying technology, the historical milestones of the industry, and the significant risks associated with digital asset management.

The Shift from Virtual Currency to Crypto Assets

In the early years of digital finance, the term "virtual currency" was the standard nomenclature used by the media and early adopters. However, as the industry matured and regulatory frameworks began to take shape, a shift in terminology occurred. In Japan, for instance, legal amendments to the Payment Services Act and the Financial Instruments and Exchange Act officially transitioned the terminology to "crypto assets." This change was intended to clarify that these digital tokens are not "currency" in the legal sense of being backed by a central government (legal tender), but are rather digital assets whose value is determined by market demand and technological utility.

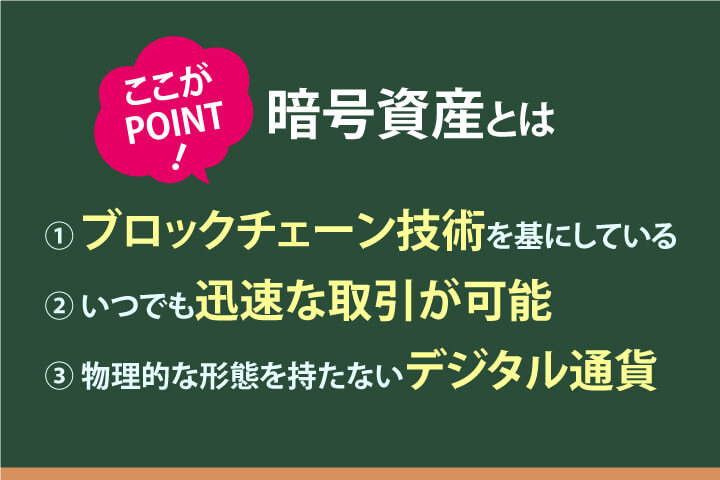

The defining characteristic of a crypto asset is its decentralized nature. Unlike traditional fiat currencies—such as the Yen, Dollar, or Euro—which are managed by central banks and commercial institutions, crypto assets utilize blockchain technology. A blockchain is a distributed ledger that records all transactions across a network of computers. This technology ensures that no single entity has total control over the system. For users, this means that transactions can occur 24/7 without the need for a bank to "approve" the transfer, and the system remains operational even if specific nodes or geographical regions experience technical failures.

A Chronological History of Digital Finance

The history of crypto assets is a relatively short but incredibly dense timeline of innovation, volatility, and paradigm shifts. Understanding how the industry arrived at its current state requires a look back at the key milestones that shaped the market.

2008–2009: The Genesis of Bitcoin

The era of crypto assets began in October 2008, when an individual or group using the pseudonym Satoshi Nakamoto published a whitepaper titled "Bitcoin: A Peer-to-Peer Electronic Cash System." This document was released against the backdrop of the global financial crisis, proposing a system where individuals could transact directly with one another without relying on financial institutions. In January 2009, the Bitcoin network went live with the mining of the "genesis block." At this stage, Bitcoin had no monetary value and was primarily a project for cryptographers and cypherpunks.

2013–2015: The Rise of Ethereum and Smart Contracts

While Bitcoin proved that digital scarcity and decentralized payments were possible, it was limited in its functionality. In 2013, Vitalik Buterin proposed Ethereum, a new blockchain that would allow developers to write "smart contracts"—self-executing contracts with the terms of the agreement directly written into code. Launched in 2015, Ethereum transformed the industry from a simple payment network into a global, programmable computer. This paved the way for decentralized applications (dApps), decentralized finance (DeFi), and non-fungible tokens (NFTs).

2020–Present: The Era of Scalability and "Ethereum Killers"

As Ethereum grew in popularity, the network became congested, leading to high transaction fees (gas fees) and slower processing times. This created a market gap for new blockchains designed for high-speed performance and low costs. Projects such as Solana (SOL), Cardano (ADA), and Avalanche (AVAX) emerged, often dubbed "Ethereum Killers." These platforms focused on scalability, attempting to solve the "blockchain trilemma"—the challenge of achieving security, decentralization, and scalability simultaneously. For example, Solana gained significant traction by offering the ability to process tens of thousands of transactions per second at a fraction of a cent per transaction, though it faced criticisms regarding its level of decentralization and occasional network outages.

Supporting Data: Analyzing Volatility and Market Performance

One of the most significant barriers to entry for new users is the extreme price volatility associated with crypto assets. To put this into perspective, a comparison between Bitcoin and traditional stock indices like the Nikkei 225 reveals a stark difference in risk profiles.

Over the past five years, Bitcoin has seen price fluctuations that often exceed 100% to 500% within a single year. While the potential for high returns is a primary draw for investors, the downside is equally dramatic. For instance, Bitcoin has experienced multiple "drawdowns" where its value plummeted by more than 50% in a matter of weeks. In contrast, the Nikkei 225, while subject to market cycles and external shocks like the 2020 pandemic, typically moves in a much more controlled and gradual manner.

Data from financial regulators suggests that the "realized volatility" of Bitcoin is often five to ten times higher than that of major fiat currency pairs or blue-chip stocks. This necessitates a strategy of "surplus capital investment," wherein individuals only invest funds they can afford to lose entirely. Professional analysts emphasize that because crypto assets are not backed by physical commodities or government guarantees, their price is driven purely by market sentiment, adoption rates, and technological milestones.

Essential Risk Management: Addressing Remittance Errors and Scams

As users move away from centralized banks toward self-custody of digital assets, they inherit the responsibility of being their own bank. This shift brings two major risks: technical errors and social engineering scams.

The Irreversibility of Remittance Errors

In traditional banking, if a user sends money to the wrong account number, there is usually a centralized authority (the bank) that can intervene, freeze the transaction, or facilitate a reversal. In the world of crypto assets, transactions are immutable. To send assets, a user must enter a "wallet address"—a long string of alphanumeric characters. If a single character is incorrect, or if assets are sent to a wallet on a non-compatible blockchain, the funds are effectively lost forever. There is no "customer support" for the blockchain to recover these assets. Experts recommend always using "copy-paste" functions and performing a small "test transaction" before sending significant amounts.

The Proliferation of Fraud and Social Engineering

The anonymity and lack of regulation in parts of the crypto space have made it a fertile ground for scammers. According to reports from Japan’s Consumer Affairs Agency, there has been a steady rise in "investment fraud" involving digital assets. These scams often follow a predictable pattern:

- Direct Messages (DMs): Scammers contact individuals via SNS platforms like X (formerly Twitter), Telegram, or Instagram.

- Guaranteed Profits: They promise "guaranteed monthly returns" of 20%, 50%, or even 100%, often claiming to have insider information or "automated trading bots."

- Initial Success: To build trust, the scammer may allow the user to "withdraw" a small amount of profit initially.

- The Exit: Once the victim invests a large sum of "seed capital," the scammer disappears, and the funds are laundered through various privacy protocols.

Official statements from the Consumer Affairs Agency emphasize a simple rule: if an investment opportunity sounds too good to be true, it almost certainly is. There is no such thing as a "guaranteed profit" in a market as volatile as crypto assets.

Broader Impact and the Future of the Web3 Ecosystem

The implications of crypto assets extend far beyond simple investment or speculation. They are the foundational layer of the Web3 movement, which seeks to return data ownership to users and eliminate the monopolies held by "Big Tech" corporations. By using tokens and crypto assets, developers can create decentralized social networks, play-to-earn gaming economies, and transparent voting systems for decentralized autonomous organizations (DAOs).

Governments worldwide are currently grappling with how to regulate this space without stifling innovation. Japan has taken a proactive stance, implementing some of the world’s strictest exchange registration requirements and consumer protection laws following high-profile hacks in the past. This regulatory clarity has made the Japanese market a unique hub for institutional interest and "stablecoin" development.

As the industry moves forward, the focus is shifting from "what" a crypto asset is to "how" it can be used to solve real-world problems. The next phase of the digital economy will likely involve the "tokenization" of real-world assets—such as real estate, fine art, and carbon credits—allowing these traditionally illiquid assets to be traded as easily as a digital coin.

For the average user, the path forward requires a balance of curiosity and caution. The Web3 era offers unprecedented financial freedom and technological potential, but it demands a high level of personal responsibility and a commitment to continuous education. By understanding the history, the technology, and the inherent risks, participants can navigate the digital frontier with confidence, ensuring that their transition into the world of crypto assets is both secure and informed.