In a landmark media roundtable held in Tokyo, Stripe, the global financial infrastructure platform, presented a comprehensive vision for the future of the digital economy, centered on the transformative potential of Artificial Intelligence (AI) and the integration of stablecoin technology. Titled "The World from the Perspective of 300 Trillion Yen Payment Infrastructure: Paradigm Shift of Digital Economy Brought by AI," the event featured key presentations from Mitsuru Hirayama, Representative Director of Stripe Japan, and Daniel Heffernan, Head of Product Development for Stripe Japan. The briefing provided a rare glimpse into the company’s internal metrics and its strategic roadmap for navigating a global economy increasingly dictated by autonomous agents and programmable money.

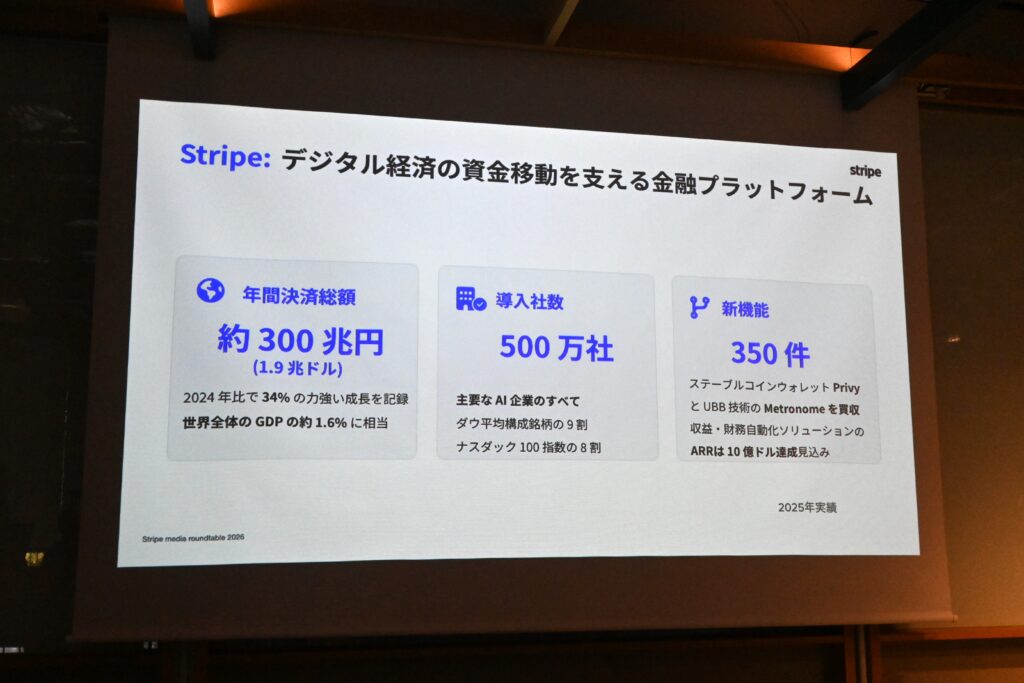

The scale of Stripe’s influence on the global economy was a primary focus of the discussion. According to data shared during the session, the total payment volume processed through Stripe’s infrastructure reached approximately $1.9 trillion USD in 2025, a figure equivalent to nearly 300 trillion Japanese yen. This massive throughput is driven by more than 5 million companies worldwide, ranging from small-scale startups to Fortune 500 giants, all of which utilize Stripe’s suite of tools to move capital across borders and industries. As Stripe Japan celebrates its 10th anniversary since its local incorporation, the company is pivoting from being a mere facilitator of credit card transactions to becoming the foundational architecture for what it terms "Agentic Commerce."

The Evolution of Agentic Commerce and the Role of AI Agents

A significant portion of the roundtable was dedicated to the concept of "Agentic Commerce"—a shift in the digital economy where AI agents, rather than human users, initiate and complete commercial transactions. Daniel Heffernan explained that the current e-commerce model, which relies on human-centric interfaces like search bars, shopping carts, and checkout buttons, is poorly suited for the speed and logic of AI.

Stripe’s internal research, conducted in March 2025 across major retail and food service enterprises, suggests that the adoption of AI agents for end-to-end purchasing is accelerating. In this new paradigm, an AI agent might be tasked with "finding the most cost-effective supply of raw materials and securing a delivery contract." For such a transaction to occur, the AI requires a payment method that is as programmable and autonomous as the agent itself. This has led Stripe to prioritize the development of infrastructure that allows machines to pay other machines without human intervention, ensuring that the friction of traditional banking hours and manual approvals does not stall the progress of automated workflows.

The Strategic Surge of Stablecoins and the Bridge Acquisition

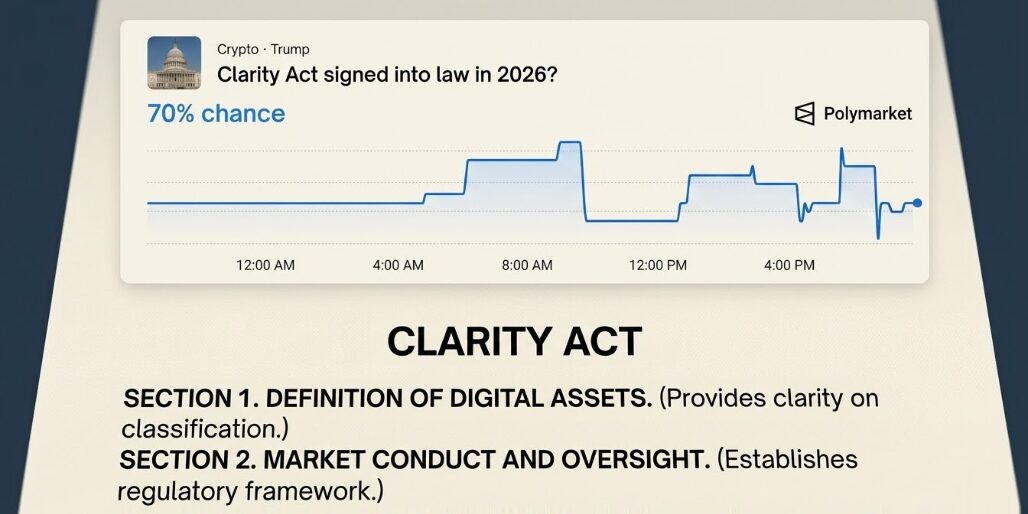

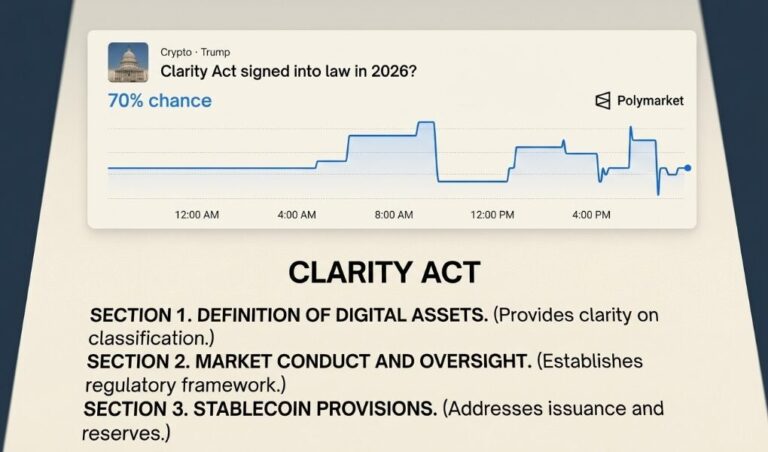

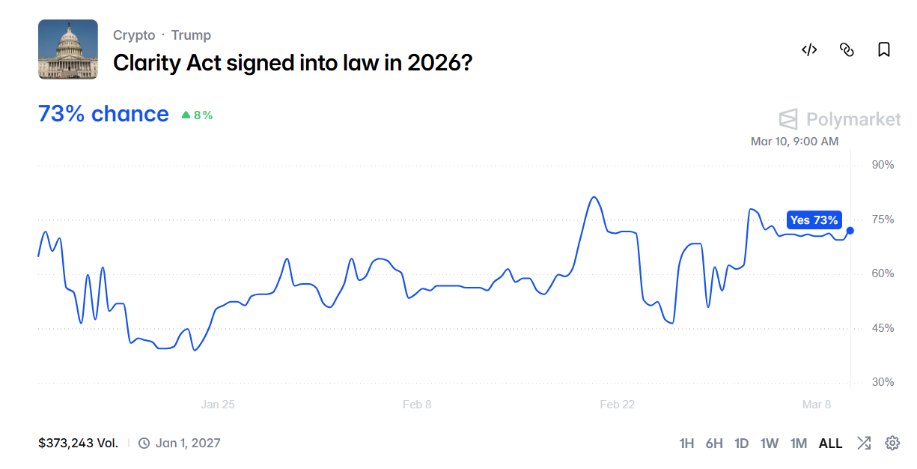

To facilitate this machine-led economy, Stripe is betting heavily on stablecoins. The company revealed that the global transaction volume of stablecoins is projected to reach approximately $4 trillion USD (60 trillion yen) by the end of 2025. Crucially, roughly 60% of this volume is now attributed to Business-to-Business (B2B) transactions, signaling a move away from speculative retail trading toward practical, utility-driven enterprise use cases.

Stripe’s acquisition of Bridge, a stablecoin payment platform, has proven to be a cornerstone of this strategy. Since the acquisition, Bridge has recorded a staggering 400% year-on-year growth. Bridge serves as an essential bridge between traditional fiat currencies and digital assets, handling the complexities of "on-ramping" (converting fiat to stablecoins) and "off-ramping" (converting stablecoins back to fiat), as well as the intricate regulatory compliance and minting processes required for global settlement.

The preference for stablecoins in the AI era stems from their 24/7 availability and near-instant settlement capabilities. Traditional cross-border wire transfers can take several days and involve multiple intermediary banks, each taking a fee. Stablecoins, operating on blockchain rails, allow AI agents to settle payments in seconds, regardless of the geographic location of the parties involved.

Introducing MPP and Tempo: Building the Open Standard for Machine Payments

During the technical segment of the roundtable, Daniel Heffernan detailed two major initiatives designed to standardize the future of payments: the Machine Payments Protocol (MPP) and Tempo.

The Machine Payments Protocol (MPP) is an open-source specification designed to enable AI agents to negotiate and execute payments autonomously. By making the protocol open, Stripe aims to prevent the fragmentation of the digital economy into "walled gardens." Heffernan emphasized that for AI commerce to thrive, there must be a common language that different AI models—whether developed by OpenAI, Google, or niche enterprise providers—can use to authorize transactions.

Complementing MPP is "Tempo," Stripe’s development of a specialized Layer 1 blockchain optimized specifically for payments. Stripe’s leadership expressed a clear recognition that existing general-purpose blockchains are often optimized for decentralized finance (DeFi) speculation or NFT minting, which can lead to high gas fees and network congestion during periods of market volatility. Tempo is being designed as a public, open-ended infrastructure that rivals the efficiency and reliability of traditional card networks like Visa and Mastercard but utilizes the transparency and programmability of blockchain technology.

"Payment is not something that one company should monopolize," Heffernan stated, highlighting the company’s commitment to an open design. He argued that to gather participants from around the world and create a truly global network, the underlying architecture must be accessible and interoperable.

Chronology of Innovation: Stripe’s Decadal Journey in Japan

The Tokyo roundtable also served as a retrospective of Stripe’s growth within the Japanese market. The timeline of Stripe’s evolution reflects a broader shift in how the financial industry views digital disruption:

- 2015: Stripe establishes its Japanese entity, focusing on simplifying online payments for the burgeoning local startup ecosystem.

- 2017-2021: Rapid expansion into the enterprise sector, with major Japanese corporations adopting Stripe to power their digital transformation (DX) initiatives.

- 2023: Stripe announces a major partnership with Visa to enhance cross-border payment efficiency.

- 2024: The acquisition of Bridge marks Stripe’s definitive entry into the stablecoin and blockchain settlement space.

- Early 2025: Stripe expands its partnership with Visa to launch stablecoin-linked cards in over 100 countries, allowing businesses to spend stablecoin balances at any merchant that accepts Visa.

- April 2025: The unveiling of MPP and Tempo in Tokyo, signaling a shift toward AI-centric financial infrastructure.

Supporting Data and Market Analysis

The data presented by Stripe aligns with broader macroeconomic trends. As global GDP increasingly shifts toward digital services, the friction inherent in the legacy financial system becomes more costly. Stripe’s $1.9 trillion volume represents a significant portion of the "Internet GDP," and the company’s focus on 2025 as a turning point for AI agents suggests a belief that the next trillion dollars in growth will come from non-human actors.

Analysts suggest that by focusing on "Machine Payments," Stripe is positioning itself to capture a market that is currently underserved by traditional banks. Banks are often constrained by "Know Your Customer" (KYC) regulations that are designed for human account holders. Stripe’s approach involves embedding compliance and identity verification into the protocol level, allowing for "Know Your Machine" (KYM) verification that satisfies regulators while enabling the speed required by AI.

Furthermore, the expansion of the Visa partnership indicates that the traditional financial establishment is no longer viewing stablecoins as a threat, but as a necessary upgrade to their own rails. The ability to bridge $4 trillion in stablecoin volume with the global reach of the Visa network creates a hybrid financial system that combines the trust of legacy brands with the efficiency of modern technology.

Broader Impact and Future Implications

The implications of Stripe’s vision are profound for both developers and traditional financial institutions. For developers, the introduction of MPP and Tempo means they can build AI applications with "built-in" wallets and payment logic, reducing the time to market for autonomous services. For traditional banks, Stripe’s move into Layer 1 blockchain development represents a direct challenge to the "settlement layer" that banks have historically controlled.

However, Stripe’s emphasis on "Open Design" suggests a collaborative rather than predatory approach. By building open protocols, they invite banks and other fintech players to participate in the ecosystem. This strategy mirrors the early days of the internet, where open protocols like SMTP for email or HTTP for the web allowed for massive, decentralized growth.

As Stripe Japan enters its second decade, the company’s trajectory is clear. It is no longer just a "checkout button" company; it is the architect of a new financial operating system. By integrating AI agents, stablecoins, and open-source protocols, Stripe is preparing for a world where the economy never sleeps, transactions happen in milliseconds, and the primary consumers are the very algorithms that power our digital lives. The successful implementation of Tempo and MPP will likely determine whether Stripe can maintain its dominance in an era where the definition of a "customer" is being fundamentally redefined.

of Ola Cabs")