Blockchain technology has emerged as the most significant architectural shift in digital data management since the inception of the internet. Often described as the "trust protocol," blockchain is the underlying mechanism that enables the existence of cryptocurrencies, non-fungible tokens (NFTs), and the broader vision of Web3. While the technology is frequently associated with volatile financial markets, its core utility lies in its ability to provide a decentralized, immutable, and transparent ledger for recording transactions and tracking assets. As global industries move toward an era of decentralized finance (DeFi) and automated governance, understanding the mechanics, benefits, and inherent challenges of blockchain has become essential for stakeholders across the public and private sectors.

The Architectural Evolution of Data: From Centralized to Distributed Ledgers

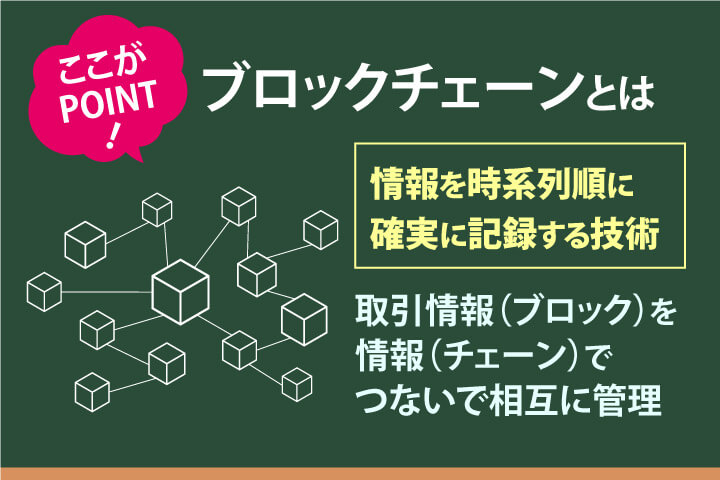

At its simplest level, a blockchain is a shared, immutable ledger that facilitates the process of recording transactions and tracking assets in a business network. An asset can be tangible—a house, car, cash, or land—or intangible, such as intellectual property, patents, copyrights, or branding. Virtually anything of value can be tracked and traded on a blockchain network, reducing risk and cutting costs for all parties involved.

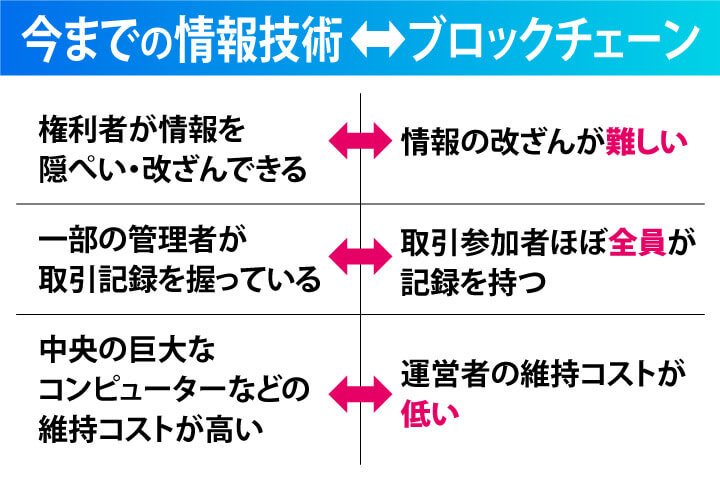

To understand the revolutionary nature of this technology, one must contrast it with traditional centralized systems. In a standard banking environment, a central authority—the bank—maintains a private database of all transactions. Customers must trust the bank’s integrity, security, and uptime to access their funds or verify their history. Blockchain disrupts this model by distributing the ledger across a vast network of computers, known as nodes. Instead of a single "giant computer" holding all the power, thousands of "small computers" share a synchronized version of the truth.

The "block" in blockchain refers to a digital collection of data. Each block contains a record of recent transactions, a timestamp, and a unique mathematical identifier called a "hash." Crucially, each block also contains the hash of the previous block, effectively "chaining" them together. This chronological link creates a dependency; if a single piece of data in an earlier block is altered, its hash changes, which breaks the link to every subsequent block in the chain. This makes unauthorized tampering immediately apparent to the entire network.

Core Characteristics: Immutability, Transparency, and Efficiency

The widespread interest in blockchain technology stems from three primary characteristics that distinguish it from legacy database systems: immutability, decentralized record-keeping, and operational cost reduction.

1. Security Through Immutability

The most lauded feature of blockchain is its resistance to modification. Once a transaction is recorded and confirmed by the network through a consensus mechanism (such as Proof of Work or Proof of Stake), it becomes nearly impossible to alter. In a traditional database, an administrator can delete or change records. In a blockchain, any attempt to change a record would require the attacker to gain control of more than 51% of the network’s computing power—a feat that is computationally and financially prohibitive for established networks like Bitcoin or Ethereum.

2. Decentralized Governance and Trust

In the current digital economy, trust is often mediated by third parties: banks for payments, lawyers for contracts, and social media platforms for identity. Blockchain removes the need for these intermediaries. Because every participant in a blockchain network has access to the same distributed ledger, there is total transparency. This "shared version of the truth" eliminates the discrepancies that often lead to disputes in traditional business settings.

3. Lowering Operational Costs

While early blockchain iterations faced criticism for high energy consumption, the technology ultimately aims to reduce the "cost of trust." By automating verification through smart contracts—self-executing code that triggers when specific conditions are met—businesses can bypass the administrative overhead associated with manual processing, audits, and third-party clearinghouses. For instance, in cross-border payments, blockchain can reduce settlement times from several days to mere seconds, significantly lowering the capital requirements for financial institutions.

Global Adoption: From Speculative Assets to Enterprise Utility

The transition of blockchain from a niche cryptographic experiment to a corporate necessity is already underway. Major global entities are integrating distributed ledger technology (DLT) to solve complex logistical and financial problems.

A recent survey of the world’s top 100 public companies revealed that a majority are actively investing in or utilizing blockchain technology. In the financial sector, VISA has integrated blockchain to streamline high-value cross-border payments, seeking to compete with the traditional SWIFT network. Similarly, Mizuho Bank in Japan has explored blockchain for trade finance to reduce the massive volume of paperwork required for international shipping.

Beyond finance, Unilever has utilized blockchain to manage its complex global supply chains. By tracking the journey of raw materials from the farm to the consumer, the company can verify sustainability claims and ensure ethical sourcing with a degree of certainty that was previously impossible. This application is particularly relevant in the modern ESG (Environmental, Social, and Governance) landscape, where consumers and regulators demand higher levels of corporate accountability.

The Blockchain Trilemma: The Great Technical Hurdle

Despite its potential, blockchain technology is not without its flaws. Vitalik Buterin, the co-founder of Ethereum, famously proposed the "Blockchain Trilemma," which posits that it is nearly impossible for a blockchain to achieve three specific goals simultaneously: Decentralization, Security, and Scalability.

Scalability vs. Decentralization

The more decentralized a network is (i.e., the more nodes it has), the longer it takes for all those nodes to reach a consensus on the state of the ledger. This often leads to slower transaction speeds. Bitcoin, for example, is highly secure and decentralized but can only process about 5 to 7 transactions per second (TPS). In contrast, traditional payment processors like VISA can handle over 24,000 TPS.

The Security Factor

To increase speed (scalability), a network might choose to limit the number of nodes required for consensus. However, reducing the number of nodes makes the network more vulnerable to a 51% attack, thereby compromising security.

Current Solutions and Innovations

The industry is currently in a phase of intense experimentation to solve this trilemma. "Layer 2" solutions, such as the Lightning Network for Bitcoin or Arbitrum for Ethereum, process transactions off-the-main-chain to increase speed while still relying on the main chain for ultimate security. Furthermore, the "Ethereum Merge" in 2022 marked a massive shift from Proof of Work to Proof of Stake, significantly reducing the network’s energy consumption by 99.9% and laying the groundwork for future scaling upgrades.

Regulatory Landscape and Official Responses

As blockchain moves into the mainstream, it has drawn the attention of global regulators. The reaction from official bodies has been a mixture of caution and curiosity. In the United States, the Securities and Exchange Commission (SEC) has focused heavily on whether certain blockchain-based assets should be classified as securities. Meanwhile, the European Union has taken a more structured approach with the Markets in Crypto-Assets (MiCA) regulation, providing a comprehensive legal framework for the industry.

Central banks are also responding by developing their own versions of the technology: Central Bank Digital Currencies (CBDCs). Unlike decentralized cryptocurrencies, CBDCs are issued by the state and maintain centralized control, yet they utilize the efficiency and transparency of blockchain to modernize national payment systems. Countries like China, the Bahamas, and Nigeria have already launched versions of digital currencies, while the Federal Reserve and the European Central Bank continue to conduct extensive research.

Broader Impact and the Future of the Digital Economy

The implications of blockchain extend far beyond money. We are witnessing the birth of Decentralized Autonomous Organizations (DAOs), where rules are enforced by code rather than executives, and the "Creator Economy," where artists use NFTs to maintain ownership and receive royalties for their work without needing galleries or record labels.

In the long term, blockchain may become a "hidden" technology, much like the TCP/IP protocols that power the internet today. Users may not realize they are interacting with a blockchain when they buy a house, vote in an election, or verify their identity online; they will simply benefit from a system that is faster, more secure, and inherently more trustworthy.

The journey of blockchain technology is characterized by rapid innovation followed by periods of consolidation and regulatory scrutiny. While the "trilemma" remains a technical challenge, the sheer volume of intellectual and financial capital flowing into the sector suggests that solutions are on the horizon. As we move further into the decade, blockchain will likely transition from a disruptive force to a standard utility, providing the essential infrastructure for a truly digital and globalized economy. The next phase of Web3 will not just be about "crypto," but about the seamless integration of decentralized trust into the fabric of everyday life.