The transition of the Ethereum network from a Proof-of-Work (PoW) consensus mechanism to Proof-of-Stake (PoS), a milestone commonly referred to as "The Merge," has fundamentally reshaped the cryptocurrency mining landscape, leading to a near-total collapse in profitability for GPU-based mining operations. For years, Ethereum served as the primary economic engine for the global mining community, offering rewards that sustained a multi-billion dollar industry of hardware manufacturers and independent miners. However, since the network successfully integrated its execution layer with the Beacon Chain, the requirement for miners to secure the network through computational power has been eliminated, leaving a massive global fleet of graphics processing units (GPUs) without their primary source of revenue.

The immediate consequence of this shift has been a "Great Migration" of hashing power. Displaced miners, seeking to utilize their existing hardware, have flooded alternative Proof-of-Work blockchains such as Ethereum Classic (ETC), Ravencoin (RVN), and Ergo (ERG). This sudden and massive influx of hashrate has triggered a dramatic spike in mining difficulty across these smaller networks. Because these chains are designed to maintain a consistent block production time, their protocols automatically adjust difficulty upwards when more computational power joins the network. Consequently, the share of rewards for individual miners has been diluted to the point where, for the vast majority of participants, the cost of electricity now exceeds the value of the cryptocurrency being mined.

The Mechanism of the Profitability Collapse

The economic crisis facing miners is rooted in the disparity between Ethereum’s original market capitalization and that of the alternative PoW coins. Before the Merge, Ethereum’s hashrate was magnitudes larger than all other GPU-minable coins combined. When that massive wave of computational power moved into smaller "alt-coin" ecosystems, it acted as a tidal wave in a small pond.

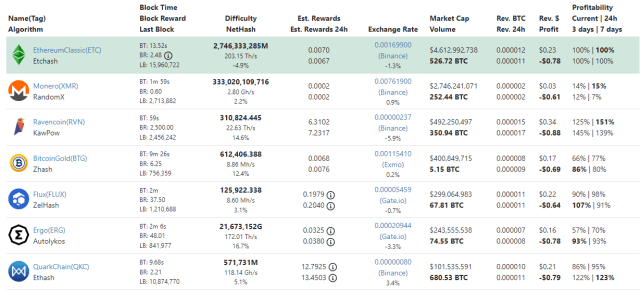

Data from the mining profitability aggregator WhatToMine illustrates the severity of the situation. For a standard mining setup utilizing three AMD RX 480 graphics cards—a once-popular mid-range choice—the daily profit for mining Ethereum Classic (ETC) has plummeted to approximately -$0.78 per hour. This calculation assumes a global average industrial electricity cost of $0.10 per kilowatt-hour (kWh). Even miners equipped with top-tier hardware, such as the NVIDIA GeForce RTX 3090 Ti, are failing to find a "break-even" point. Under the same electricity cost assumptions, an RTX 3090 Ti currently nets an hourly profit of roughly -$0.50.

This negative yield indicates that miners are effectively paying out of pocket to secure these networks, a strategy that is unsustainable for all but the most well-capitalized operations or those with access to near-zero-cost electricity. For the average home miner or small-scale commercial farm, the "Merge" has effectively signaled the end of GPU mining as a viable business model in the current market environment.

Chronology of the Transition: From Beacon to Merge

The road to the current mining crisis began years ago, but the timeline accelerated significantly in 2022. Understanding the chronology is essential to grasping why the market was unable to absorb the displaced hashrate.

- December 2020: The Beacon Chain launched, introducing the Proof-of-Stake consensus layer to the Ethereum ecosystem. This allowed users to begin staking ETH, though the main network continued to run on Proof-of-Work.

- Early 2022: Ethereum developers began successful tests on various testnets (Ropsten, Sepolia, and Goerli), signaling that the transition to PoS was imminent.

- August 2022: The "Bellatrix" upgrade was announced, setting the stage for the final Total Terminal Difficulty (TTD) that would trigger the Merge.

- September 15, 2022: The Merge officially took place. As the TTD was reached, the Ethereum network ceased all PoW operations. Within minutes, the Ethereum hashrate dropped to zero.

- September 16–18, 2022: Hashrates on Ethereum Classic, Ravencoin, and Ergo spiked by 300% to 500% almost instantly. Mining difficulty adjusted upward accordingly, and profitability for these coins crashed into negative territory within 48 hours of the Merge.

The Role of Ethereum Classic and Failed Forks

Ethereum Classic (ETC) was widely viewed as the natural successor for displaced miners. As a legacy version of Ethereum that maintained the PoW consensus after the 2016 DAO hack, it shares a similar hashing algorithm (Etchash) with the original Ethereum (Ethash), making the transition seamless for hardware. In the months leading up to the Merge, Ethereum co-founder Vitalik Buterin even suggested that miners who preferred PoW should migrate to ETC, stating, "It’s a very fine chain."

However, the sheer volume of the migration overwhelmed ETC. Its market capitalization and trading volume are only a fraction of Ethereum’s, meaning it cannot generate enough block rewards in dollar terms to support the millions of GPUs that were previously mining ETH.

In addition to ETC, a group of miners and developers attempted to preserve the original PoW chain by creating a hard fork known as EthereumPoW (ETHW). While this chain launched shortly after the Merge, it struggled with technical glitches, a lack of widespread exchange support, and a rapidly declining price. Without a robust ecosystem of decentralized applications (dApps) and stablecoins, ETHW has failed to provide a profitable refuge for the mining community.

Industry Reactions and the "GPU Glut"

The reaction from the mining industry has been one of forced capitulation. Major mining pools, such as Ethermine, the world’s largest Ethereum pool at the time, announced they would not support any PoW forks and instead launched staking services to adapt to the PoS model.

Hardware manufacturers like NVIDIA and AMD are also feeling the ripple effects. For several years, the high demand from miners kept GPU prices at record highs, often double or triple the Manufacturer’s Suggested Retail Price (MSRP). Following the Merge, the secondary market has been flooded with used graphics cards as miners attempt to recoup their capital investment. This "GPU glut" has led to a sharp decline in retail prices, benefiting the gaming community but signaling a period of reduced revenue for hardware companies that had grown accustomed to the mining boom.

Experts in the field have noted that the environmental narrative played a significant role in the community’s support for the Merge. By switching to PoS, Ethereum reduced its energy consumption by an estimated 99.95%. While this is a victory for the network’s ESG (Environmental, Social, and Governance) profile, it has left PoW advocates arguing that the security provided by physical energy expenditure is being sacrificed for efficiency.

Broader Implications and Future Outlook

The current state of negative profitability raises questions about the long-term viability of PoW for any coin other than Bitcoin. Bitcoin utilizes ASIC (Application-Specific Integrated Circuit) hardware, which is fundamentally different from the GPUs used for Ethereum. Therefore, the Ethereum miners cannot simply switch to Bitcoin; they are locked into the "Alt-coin" ecosystem.

For a PoW coin to become profitable again, one of two things must happen:

- Mass Capitulation: A significant percentage of miners must turn off their machines, causing the hashrate and difficulty to drop until the remaining miners can break even.

- Price Appreciation: The market price of coins like ETC, RVN, or ERGO must increase by several hundred percent to match the current difficulty levels.

Currently, neither scenario seems imminent. With the global economy facing inflationary pressures and rising energy costs, the "overhead" for mining is increasing just as the rewards are shrinking.

Ethereum Price Analysis Post-Merge

As for the asset itself, Ether (ETH) has experienced a "sell the news" reaction in the wake of the Merge. At the time of writing, the price of Ether is hovering around the $1,400 mark, representing a decline of approximately 6% over the past week. Despite the successful technical execution of the Merge, broader macroeconomic headwinds—including interest rate hikes by the Federal Reserve—have weighed heavily on the crypto market.

While the reduction in ETH issuance (often referred to as the "triple halving") is expected to provide long-term deflationary pressure on the supply, the immediate post-Merge period has been characterized by volatility and a lack of clear bullish momentum. Investors appear to be waiting for the network to prove its stability under the new PoS consensus before committing to new long positions.

In conclusion, the Ethereum Merge has achieved its technical goals but has left a trail of economic disruption in the mining sector. The "death" of GPU mining may be an exaggeration in the long run, but for the foreseeable future, the era of easy profits from home-based mining rigs appears to have come to an end. The industry now enters a period of consolidation, where only those with the most efficient hardware and the cheapest energy sources will survive.